Estate Planning for Retirees & Mature Families

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

How do you start the conversation with your family when you are reaching that time in your life to move away from the daily business or work life?

Once your children are grown and have been on their own, they should understand better how to progress with these important life decisions. So, the best advice is to be open and frank with the conversation. Here are some helpful tips for approaching the subject.

The kids have grown up and they’re adults now and the dependency on us as parents has waned. When I think about estate planning for retirees and mature families vs. younger families, there are certainly several different issues that arise your family dynamics become increasingly important.

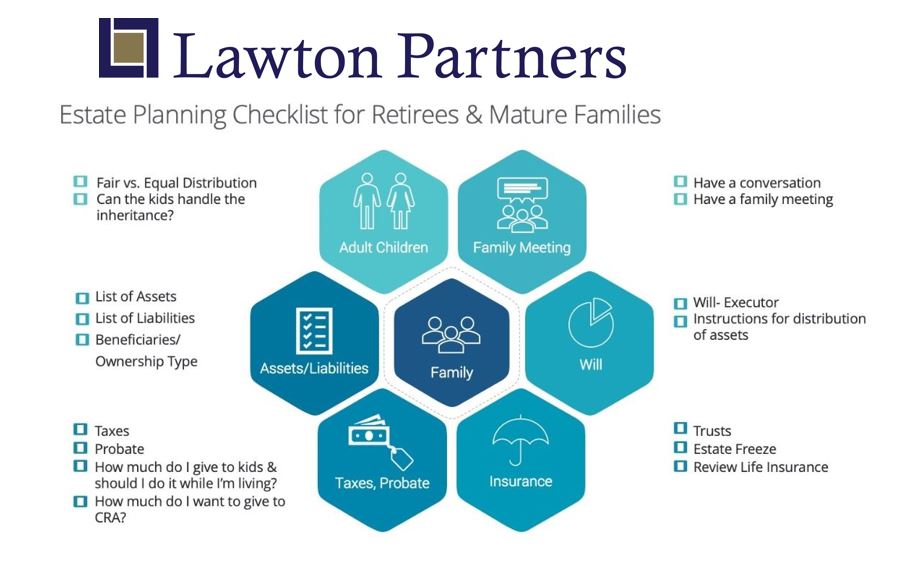

The graphic checklist below will help guide you through the questions you need to address and how to implement the actions or tools needed to proceed in a manner that is fair and equitable for all. (see the graphic attached)