Macroeconomic Perspectives: In 2023 — A Slower Economy? Keep Perspective

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

“The views and opinions expressed in this article are those of the author and do not necessarily reflect the position of Pattison Media and this site.”

As we move into 2023, there is little doubt that we should anticipate a slower economic environment here at home. With the ongoing pursuit by the central banks to bring down inflation, it is expected that rates will continue to increase, at least for the near term. These rate hikes are intended to slow the economy, and this is expected to eventually bring inflation under control.

For many months, both Canadian and U.S. central banks have indicated that they are willing to push economies into recession to prevent inflation from becoming entrenched, and the media has been busy evoking worry over the potential for an earnings recession or a full-blown economic recession. As one economist put it, “if we do have a downturn…it will be the most well-telegraphed recession in modern memory.”1

Keep Perspective…

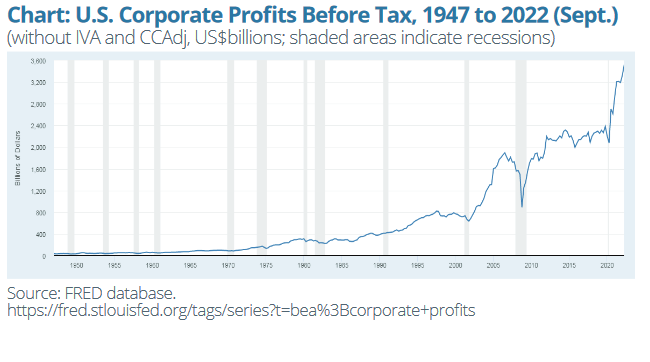

While slowing the economy will put downward pressure on corporate earnings, there may be reasons to

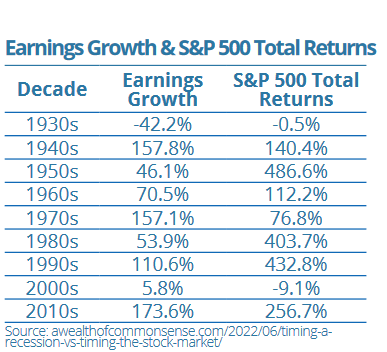

keep perspective. Over the longer term, the stock market is driven by fundamentals such as corporate earnings.