School Days

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

The ABCs of using RESP funds.

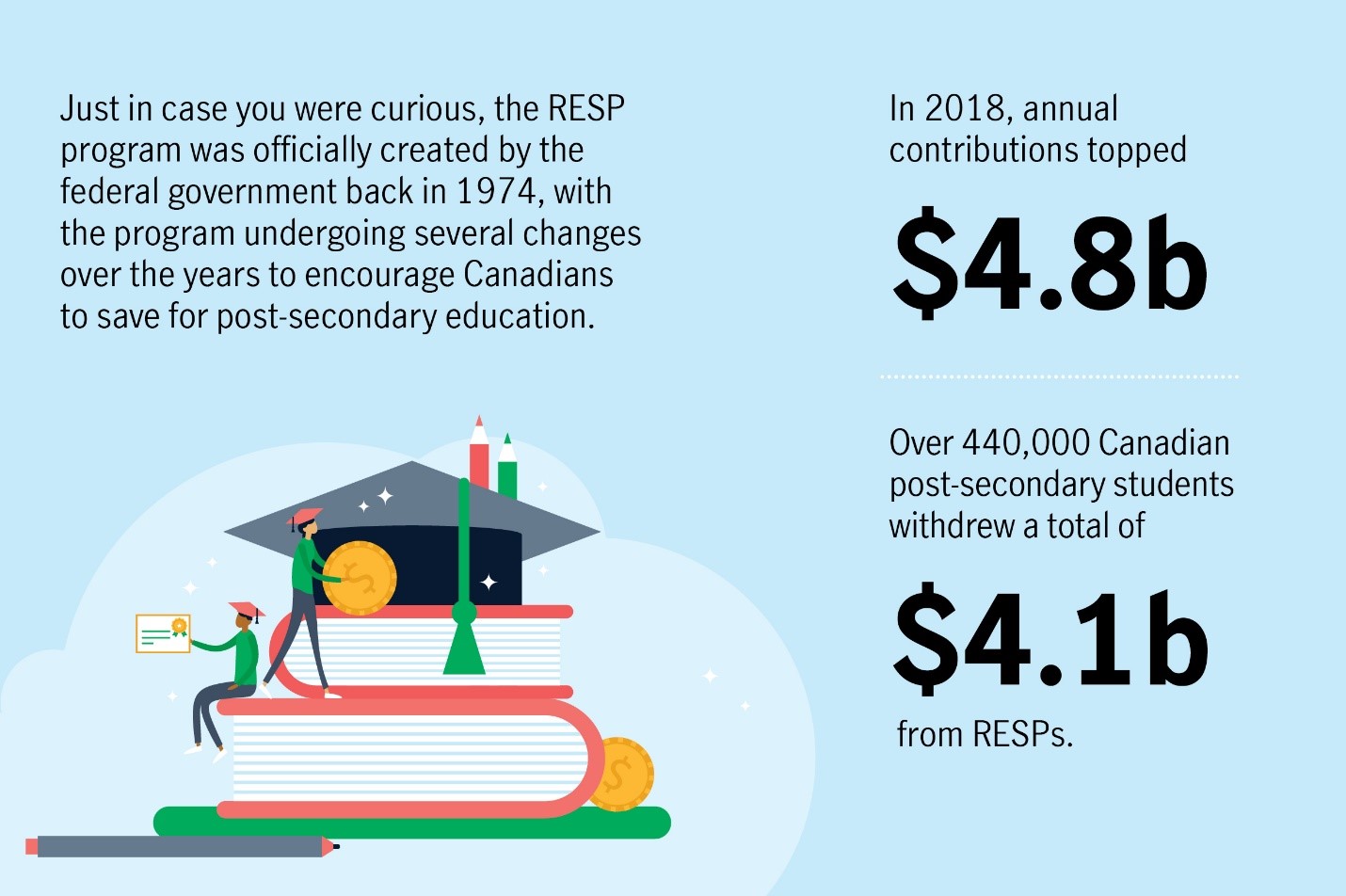

Your wee babes have grown into young adults ready to take on the world – or at least head to, post-secondary education. Knowing that college and university come with a hefty price tag, you have faithfully made contributions over the years into a Registered Education Savings Plan (RESP). Now that it’s time to use these funds to help your kids or grandkids with tuition, the next steps may feel somewhat overwhelming. Consider this your primer on how to use these savings – including the “what now” scenario if a post-secondary dream falls flat.

RESP refresher

Anyone can open an RESP for a child, whether a parent, grandparent, other relative or friend. There are different types of RESPs. An individual plan has one beneficiary. A family plan can have many beneficiaries, which is ideal for families with more than one child. Group plans have multiple beneficiaries and multiple contributors, and are generally managed as scholarship funds.